The Growth of Stablecoins

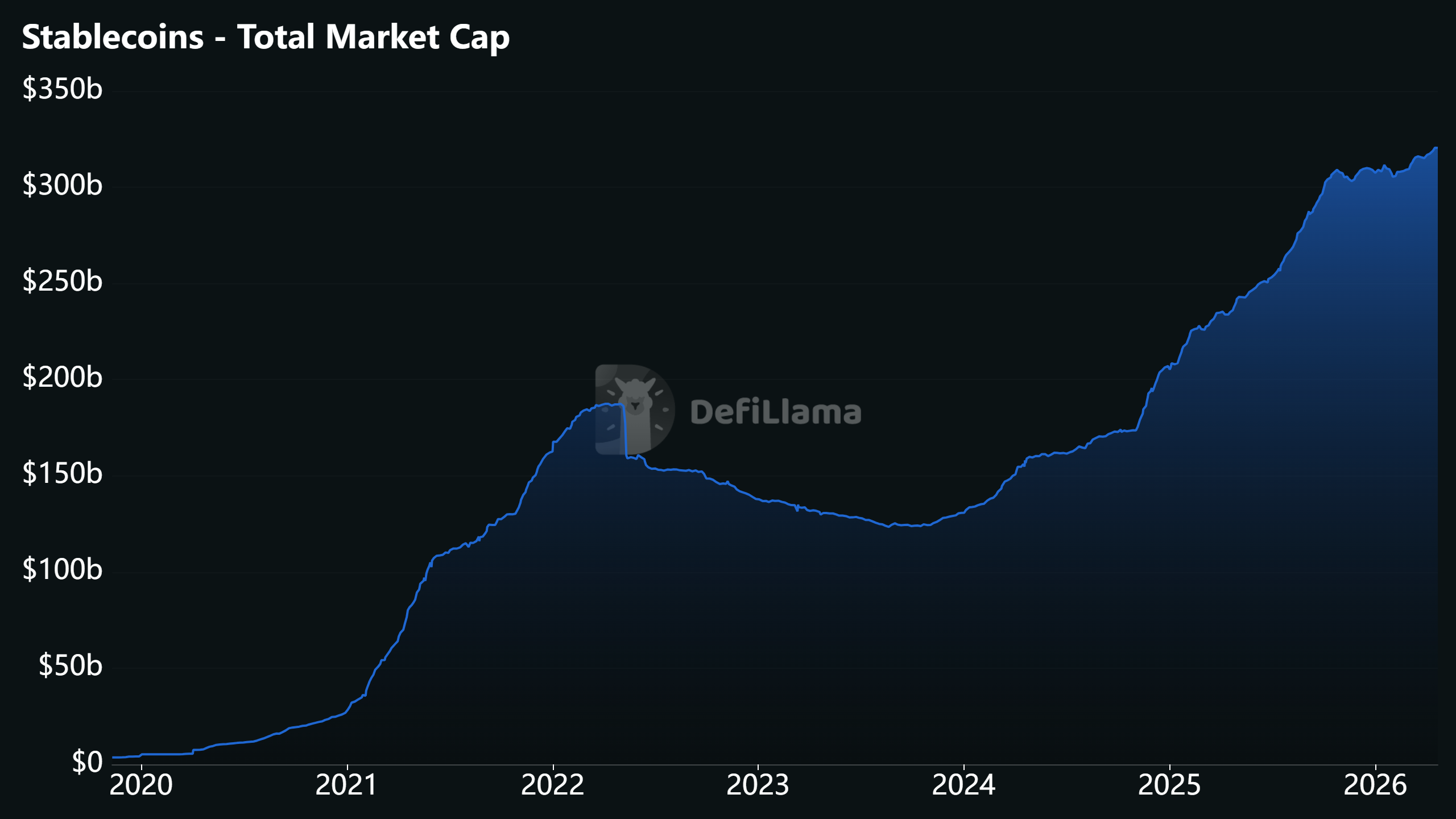

The total stablecoin market has now grown to more than $320 billion. Back in 2020, that figure was still below $10 billion. This makes it clear that stablecoins are no longer just a tool for traders. They are increasingly functioning as digital dollars operating on blockchain rails.

From Speculative Crypto Trading to Hundreds of Billions

The growth of stablecoins has gone through several distinct phases, but since the end of 2023 it has followed a steady upward trajectory. By the end of 2024, the market crossed the $200 billion mark for the first time. By mid-June 2025, it had already reached $251.7 billion. In September 2025, that figure rose to nearly $300 billion. Today, DefiLlama shows a total market value of more than $320 billion.

That pace of growth shows that stablecoins are steadily gaining market share, both within crypto and across broader payment and settlement networks. This is no longer a temporary trend. It is a segment that is developing into a structural building block of digital financial infrastructure.

One important difference compared to previous years is where that growth is coming from. For a long time, stablecoins were often used as a temporary safe haven for crypto investors. Investors would sell volatile positions, move into stablecoins, and wait for a new entry point. That function still matters, but it now explains a smaller share of the overall picture.

More and more stablecoins are now being used for their own use case. Think of international payments, settlement between companies, treasury management, and fast digital transactions outside traditional banking rails. In other words, stablecoins are no longer only being held to re-enter the market later. In many situations, they are simply being used because they are more efficient.

Growing Adoption

The rise of stablecoins is becoming increasingly visible in practice. Where the market was initially driven mainly by activity within crypto itself, we are now seeing companies, fintechs, and payment platforms actively integrating stablecoins into their services.

Stablecoins are increasingly being used for real economic activity. This includes international payments, cross-border settlement, and the more efficient movement of capital between companies and markets. Because stablecoins are available 24/7 and transactions can often be processed faster and at lower cost than through traditional infrastructure, their appeal is growing well beyond the crypto market.

Major players are also actively building around them. Stripe rolled out stablecoin-powered accounts for businesses in more than one hundred countries. PayPal further expanded PYUSD and directly linked it to international payments and faster settlement. Circle, through its payment network, also took further steps toward broader stablecoin usage in global payments.

This shows that stablecoins are increasingly being seen as a practical payment and settlement layer for real-world economic use cases.

What Makes Stablecoins So Attractive?

The appeal of stablecoins lies in the combination of a relatively stable value and the efficiency of blockchain technology. That is exactly why they are gaining traction among both businesses and consumers.

Key advantages of stablecoins include:

Fast transactions: Settlement of transactions and payments can often take place almost instantly, making them faster and more direct than traditional financial infrastructure.

Low transaction costs: In many cases, costs are lower than with traditional, especially international, payments.

24/7 availability: Stablecoins do not have opening hours. Settlement can take place day and night, including across borders and time zones.

Programmability: Stablecoins can be integrated into smart contracts, automated payments, and new digital financial applications.

Better access to dollars: In countries with weaker local currencies, dollar-denominated stablecoins can offer a practical alternative for saving or spending.

Greater utility for businesses: Stablecoins offer growing operational benefits for treasury management, cross-border settlement, and working capital management.

It is precisely this combination that makes stablecoins so interesting. They combine the reliability of traditional currencies with the speed and flexibility of blockchain technology.

Who Dominates the Stablecoin Market?

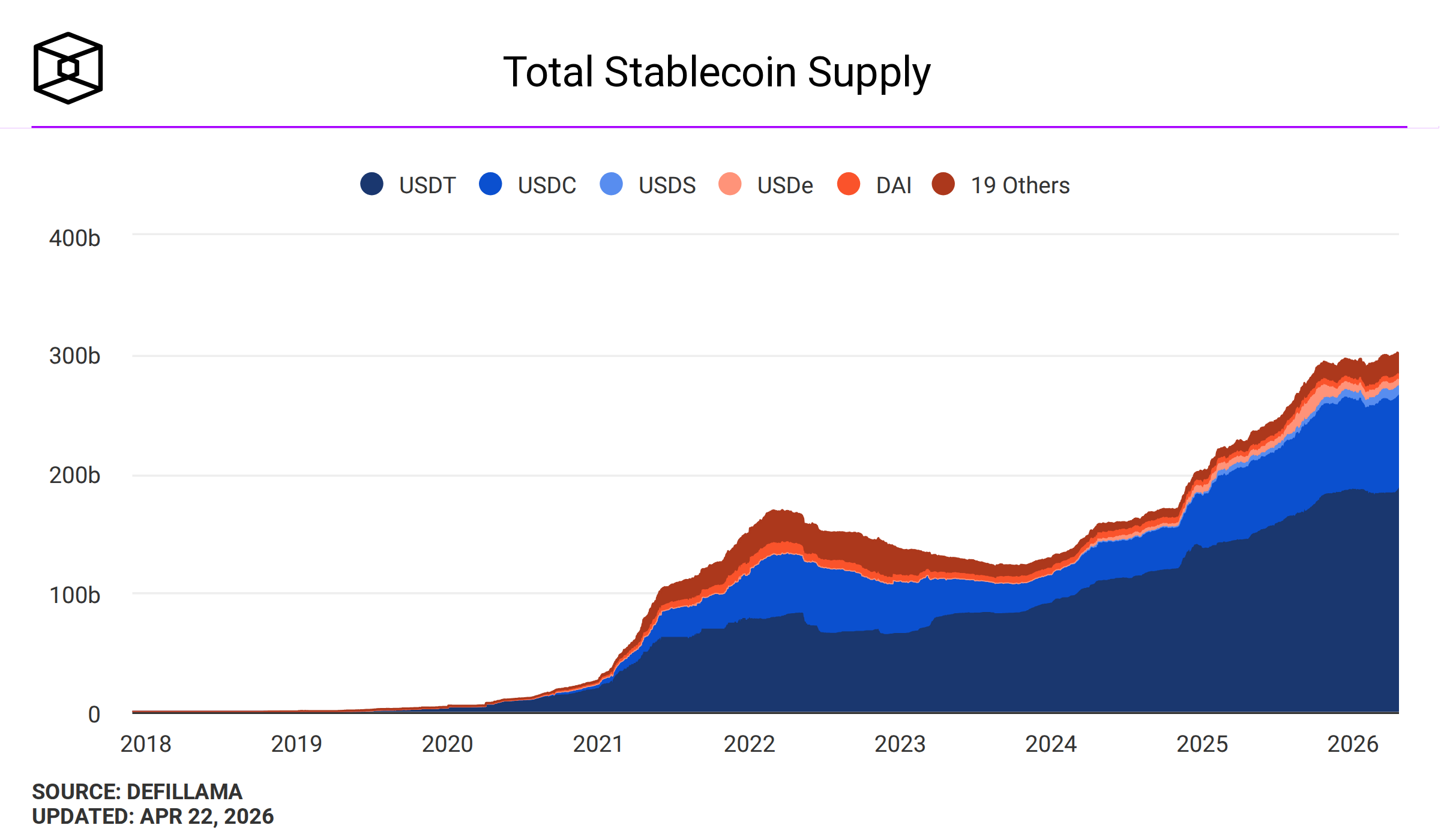

Although the stablecoin market is growing rapidly, that growth is still concentrated among a limited number of major players. The market is clearly dominated by dollar-denominated stablecoins, most notably USDT (Tether) and USDC (Circle).

USDT still holds the largest market share and remains the dominant player in the segment. USDC follows as the clear number two and plays an especially important role in more institutional applications and regulated infrastructure. Together, these two stablecoins account for by far the largest share of the total market.

That is not surprising. The US dollar remains the world’s dominant reserve currency and also plays a central role in the digital economy. As a result, it is natural for many users, companies, and platforms to choose dollar stablecoins as the foundation for transactions, settlement, and liquidity management.

At the same time, this concentration also shows that there is still plenty of room for the market to broaden further, both in terms of issuers and currencies.

The Growing Market for Euro Stablecoins

While the stablecoin market is still heavily dominated by dollar products today, interest in euro stablecoins is also increasing. This segment remains relatively small, but that is exactly what makes it worth watching.

In Europe, there is growing demand for digital euro alternatives that can be used for settlement, payments, and on-chain financial applications without direct dependence on the dollar. Given the current uncertainty in the international landscape, that need is becoming increasingly clear. The dollar’s exchange rate against the euro has been volatile, which can create unfavorable conditions for European investors and businesses.

The euro stablecoin market is still in its early stages, but there is clearly active development underway. Various banks, fintechs, and financial institutions are exploring how these products can be integrated into their own infrastructure. Dutch banks are also involved. A group of 12 European banks, including ING, is working under the name Qivalis on its own euro stablecoin.

The Future of Stablecoins

Our expectation is that the growth of stablecoins will continue in the years ahead. Not because they will replace existing payment rails overnight, but because they function demonstrably better in specific areas. Think of cross-border payments, always-on settlement, programmable money flows, and more efficient digital commerce.

At the same time, the traditional financial world is becoming increasingly intertwined with blockchain technology. Stablecoins form a logical bridge between the two. They combine familiar value with new infrastructure and make it possible to move money faster, more cheaply, and with greater flexibility.

Where stablecoins were once seen mainly as a tool within crypto, they are now increasingly developing into an independent financial use case. That is exactly where their strength lies. Stablecoins are starting to look like a fundamental building block of a new financial system, in which traditional infrastructure and blockchain technology become ever more closely connected.