ZK Series: The 1-Year evolution of the ZK Fund

One Year of DNMN / ZK Fund

When we first launched the Delta-Neutral & Market-Neutral Fund (DNMN), we did so in response to a clear need we saw among many investors: access to the opportunities in the crypto market, while being less dependent on purely rising markets. In a market that trades 24/7 and is known for its volatility, there was a clear demand for greater stability, better risk control, and a strategy that could also add value in less favorable market conditions.

Because of the benefits this offers, it was also decided that part of the Dutch Hodl funds could be allocated to this fund. What has changed over the past year is the way we give substance to that objective.

The transition from the DNMN Fund to the ZK Fund in October 2025 was not a cosmetic change, but a fundamental step forward: a new strategy, a new structure, and a much stronger foundation for generating sustainable returns.

Why We Started DNMN

The DNMN Fund was launched based on the conviction that market-neutral strategies can play an important role within crypto. Many investors want to benefit from the opportunities this market offers, while also looking for an approach that is less sensitive to major drawdowns and abrupt shifts in sentiment.

With DNMN, we aimed to meet that need. The fund was designed as a strategy that did not rely entirely on market direction, but instead sought to generate returns from inefficiencies and market structure. In doing so, it laid the foundation for what would later evolve into the ZK Fund. Read more about the launch of the ZK Fund here.

Where the Old Strategy Reached Its Limits

The original DNMN setup was largely built around a cash-and-carry approach. In the early stages, this was a logical and effective way to generate market-neutral returns. As the market continued to develop, however, the limitations of that approach became increasingly clear.

The main challenge was that our edge relative to other players in the market began to decline. At its core, cash and carry is relatively easy to replicate. As more participants started targeting the same opportunities, competition increased and returns compressed. Especially in a market where more professional and semi-professional players are becoming active, it becomes harder to remain differentiated on that basis alone.

In crypto, alpha is never permanent. As soon as a strategy becomes more widely adopted, returns often decline. That meant we had to keep evolving: away from a fund that relied primarily on one type of opportunity, and toward a broader and more robust strategy framework.

DNMN vs. ZK Fund

The difference between DNMN and the ZK Fund is significant. In practice, DNMN was a relatively narrow market-neutral strategy, while the ZK Fund has been built to be far broader and more advanced.

Where the old strategy relied mainly on cash and carry, we now combine market-neutral strategies with high-Sharpe strategies. We look across different markets, different types of inefficiencies, and different algorithmic applications. We hold tokens where doing so provides a strategic advantage, and where relevant, we also focus on high-frequency trading.

The objective is straightforward: to build a more robust fund. Different strategies should complement one another. If one approach is less favorable in a certain period, another should be able to offset it. That is the only way to work toward more consistent returns and a structurally higher Sharpe ratio.

Significant Improvement in Performance

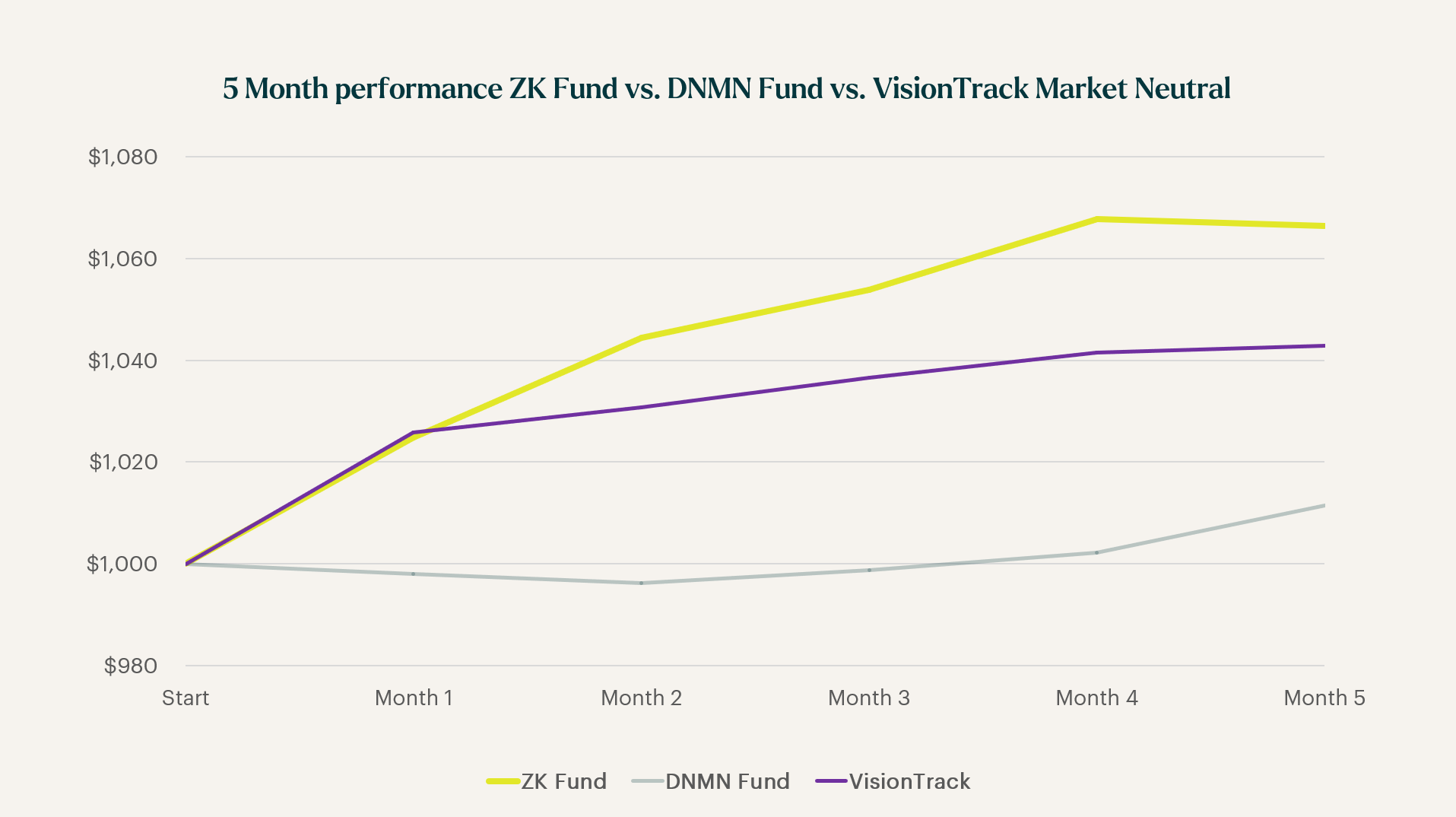

This transition has not only paid off strategically, but also directly in the results. While DNMN generated an average net monthly return of approximately 0.3%, the ZK Fund has delivered 1.25% net per month since October. That is a significant improvement and confirms that the new setup is clearly superior to the old one.

Importantly, this improvement is not the result of taking on more risk, but of a better combination of research, infrastructure, execution, and strategic diversification. The stronger returns are also reflected in the fund’s structural outperformance versus the VisionTrack Market Neutral Index, an index that tracks the returns of other market-neutral funds. For us, that is an important confirmation that the new approach is proving itself in practice and that we clearly maintain an edge over other players in the market.

Below, the performance of the ZK Fund is shown since the start of the strategy in October. The returns shown reflect the performance of the ZK Fund and the VisionTrack Market Neutral Index for the period from October 2025 through February 2026. For DNMN, this refers to the performance from March 2025 through July 2025.

The Role of Infrastructure

A significant part of that improvement comes from what we have built behind the scenes. Over the past months, we have invested heavily in the development of our execution engine and the further optimization of our infrastructure.

Our internal latency is now below 15 microseconds. Tick-to-trade — from receiving market data to executing an order — is below 200 microseconds. These are serious speeds, and they are essential in a market as volatile as this one. They can make the difference between a successful trade and a missed opportunity.

This infrastructure allows us to trade volume more efficiently, move in and out of positions more intelligently, and reduce costs further. The fact that we have been able to build this in-house over the past years gives us a significant advantage and a strong foundation for further optimization.

Not Yet Where We Want to Be

At the same time, this is not the end point. I am very pleased with the steps we have taken, but I am not yet satisfied with where we are today. A net monthly return of 1.25% is strong, but our ambition is higher. I would like to grow that to more than 2% net per month.

That next step will have to come from further improvements in infrastructure and execution, but also from expanding our range of strategies and algorithms. We remain highly selective in that process. New strategies will only be added if they meet our requirements in terms of return, risk, scalability, and correlation.

Proud of the Team

Looking back on the past year, what I am most proud of is what the team has built. The transition from DNMN to ZK was a major step from a strategic, technical, and operational perspective. It required a great deal of research, development, and discipline.

We deliberately chose not to hold on to a model whose edge we saw declining, but instead to keep building toward something better. That takes conviction, speed, and a team that is willing to keep improving itself continuously.

Looking Ahead

Looking ahead, I have a great deal of confidence in the ZK Fund. In a market where macro uncertainty, geopolitical tensions, and shifting sentiment are making investors more cautious, the demand for reliable returns with less dependence on market direction remains strong.

I expect that we can deliver a strong average annual return this year. That does not mean every month will look the same, but it does mean we are building a fund with fewer weak months, limited downside, and increasingly consistent returns.

The step from DNMN to ZK was therefore much more than a rebranding. It was a necessary evolution toward a better fund: broader in strategy, stronger in infrastructure, and clearly better in performance. We are pleased we made that move, but we are far from satisfied. The real ambition lies in what we continue to build from here.

Conclusion

Generating returns in a downward market requires a different mindset. Less focus on “the market must go up,” and more focus on structure, inefficiency, risk management, and stability. In these phases, the limitations of purely directional investing become visible, while market-independent strategies can prove their value.

For investors, this means that a good strategy should not only work in bull markets. The true quality of a fund or portfolio often reveals itself when markets come under pressure. And that is exactly where the relevance of market-neutral and high-Sharpe approaches emerges: seeking returns where others mainly see risk.